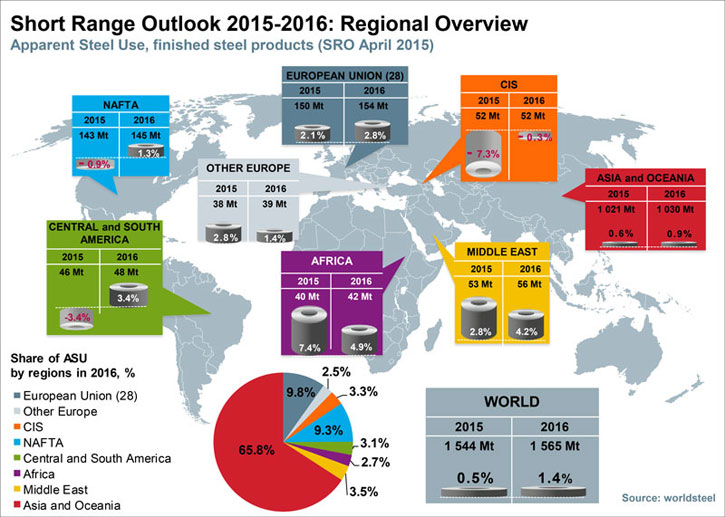

The World Steel Association (worldsteel) today released its Short Range Outlook (SRO) for 2015 and 2016. worldsteel forecasts that global apparent steel use will increase by 0.5% to 1,544 Mt in 2015 following growth of 0.6% in 2014. In 2016, it is forecast that world steel demand will grow by 1.4% and will reach 1,565 Mt.

The outlook for the steel industry suggests slow growth for global steel demand

Commenting on the outlook, Hans Jürgen Kerkhoff, Chairman of the worldsteel Economics Committee said, “We are releasing a restrained growth outlook for the global steel industry mainly due to the deceleration in China. The outlook also reflects the influence of major structural adjustments in most economies, particularly owing to limited investment growth post 2008. As these changes take effect, the steel industry will experience a slower pace of growth, it will focus on operational efficiencies and on the value that steel products generate for customers and society.”

“While we continue to face some downside risks coming from some parts of Europe – geopolitical instability, international capital flow volatility and the economic slowdown in China – the impact of these risks has come down. We have also started to see some encouraging developments. We hear increasingly positive news from developed economies, especially signs of firming recovery momentum in the Eurozone. In the developing and emerging world, we see increased optimism about India and growth in steel use in some MENA and ASEAN countries. While these developments will not be enough to counterbalance the deceleration of China, we expect to see gradually improving growth prospects beyond 2016,” Kerkoff concluded.

An interesting factor which has become increasingly apparent is that in some developing economies the steel markets are beginning to exhibit the characteristics of mature markets.

China

Chinese steel demand in 2014 saw negative growth for the first time since 1995 due to the government’s rebalancing efforts that had a major impact on the real estate market. This situation is likely to remain unchanged in the short term and Chinese steel use will continue to record negative growth of -0.5% in both 2015 and 2016. In the medium term no strong rebound is expected. Some uncertainty remains regarding the impact of government measures aimed at stabilising the decelerating economy.

The rebalancing of the Chinese economy is inevitable as China enters its next stage of development, but it will take time. In the short term, it has global consequences for the steel industry in terms of trade flows and possible intensification of trade frictions, resulting from significant increases in steel imports in many economies during 2014.

Oil prices

The sharp decline in oil prices influenced the forecast, though its impact varies between countries. On the one hand, it has a negative impact on steel demand for infrastructure investments financed from oil revenues; on the other hand it helps business sectors and consumers in oil importing countries, thus creating better growth prospects. As inflationary pressure is alleviated, further relaxation of monetary policy by the Central Banks is possible in countries with high inflation, which will eventually strengthen the recovery of underlying real steel use. As economies adjust to lower oil prices, it may lead to reduced demand for steel in some economies in the short term, but should support economic growth and demand for steel in the medium term.

The developed world

The developed world showed growth in steel demand of 6.2% in 2014 on the back of strong US fundamentals and a firming EU recovery. However, growth in the developed world is set to moderate in 2015 due partly to the high base effect, but also less favourable steel market environments in the US, Japan and South Korea. The recovery in the EU, although becoming regionally broader based, is still constrained by weak investment activity and high unemployment. Steel demand in the developed economies will grow by 0.2% in 2015 and by 1.8% in 2016.

The developing world (excluding China)

The developing economies (excluding China) posted low growth of 2.3% in 2014, in particular because of the continued deterioration in the Brazilian and Russian steel markets. Growth momentum in the developing economies is expected to remain generally weak in 2015, however, we expect positive growth in some economies such as India, Indonesia, Vietnam and Egypt, where steel markets are still developing. Steel demand is expected to grow by 4.0% in 2016 after growing by 2.4% in 2015.